Most people believe they will recognize lifestyle inflation when it arrives. They imagine a dramatic moment: the luxury purchase, the oversized mortgage, the sports car. But as Investopedia defines it , lifestyle creep is a gradual increase in spending as a person’s income rises, often without intentional planning. It sneaks. Former luxuries become necessities not through a vote, but through repetition. By the time you notice, the new standard of living has hardened into concrete. The apartment feels essential. The delivery app feels inevitable. The upgraded wardrobe feels like maintenance, not indulgence.

The critical distinction is timing. Year 1 is visible. You can point to the receipts. Year 5 is invisible. The spending has been absorbed into your baseline, and your baseline now requires the higher income just to break even. Research from Jemma Financial found that almost 50% of people who earn $100,000 or more annually live paycheck to paycheck. The raise did not create security. It created a higher treadmill speed. Understanding the Year 1 versus Year 5 progression is the only way to step off before the momentum carries you into a standard of living you never actually chose.

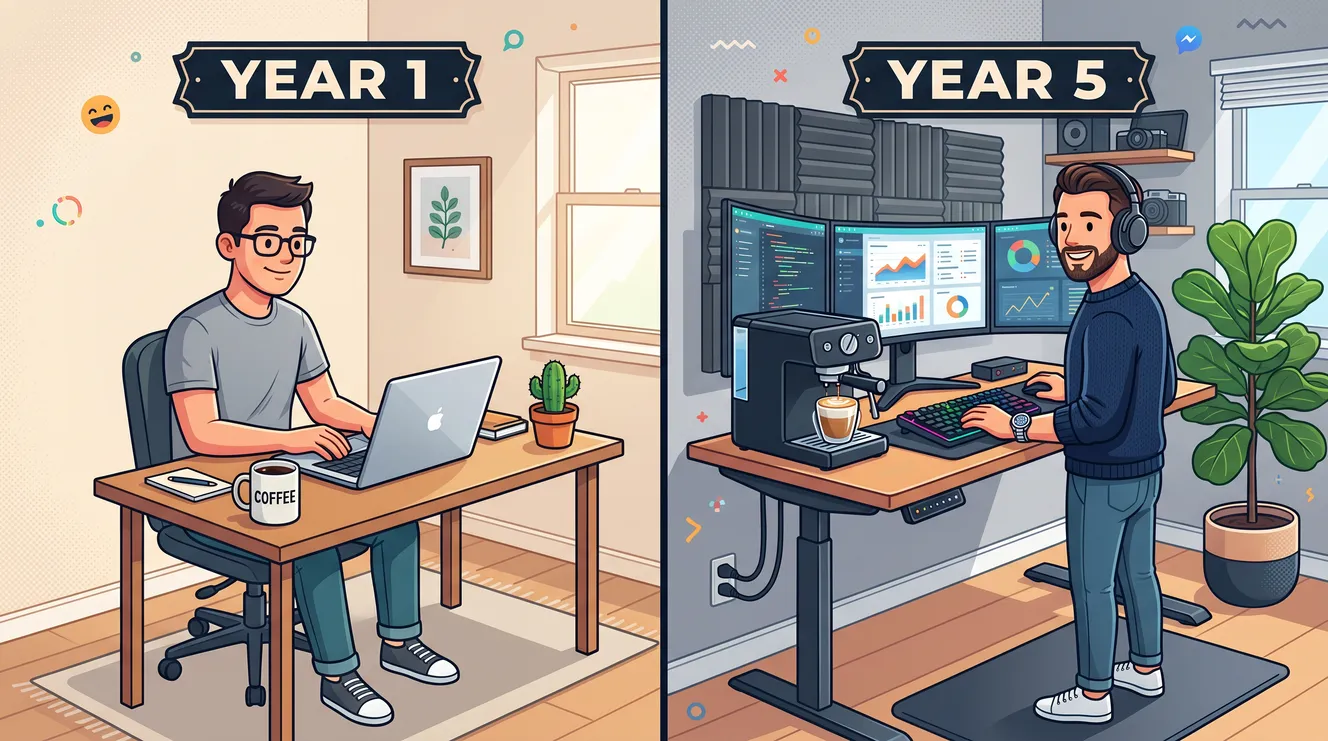

Year 1: The Visible Upgrade Phase

In the first year after a raise, lifestyle inflation is unmistakable. You make conscious, celebratory decisions. The old couch goes to the curb. The thrift-store wardrobe gets phased out. You upgrade from the studio to the one-bedroom, from the compact to the sedan, from the bus pass to the ride-share budget. These are not accidents. They are deliberate rewards for years of effort, and on some level, they are deserved. The problem is not the upgrade. The problem is the absence of a boundary.

Year 1 spending is characterized by one-time purchases that feel like events. You buy the new mattress. You book the vacation. You replace the laptop. Each decision is discrete, defensible, and often necessary. The mattress was ten years old. The laptop was slowing your work. The vacation was your first in three years. Because these purchases are event-based, they do not feel like inflation. They feel like catching up. And because they are visible, they are easy to rationalize to yourself and others.

What most people miss in Year 1 is the simultaneous shift in recurring spending. The raise enables a new apartment, which brings a higher utility bill, a parking fee, and renter’s insurance on a more expensive policy. The new car brings higher payments, premium fuel requirements, and costlier maintenance. Fidelity’s analysis notes that lifestyle creep happens when your spending expands along with your income but savings fall by the wayside. The one-time purchases are the headline. The recurring obligations are the fine print that compounds.

Social signaling also peaks in Year 1. You are newly aware of your income bracket, and you begin to notice where your old habits no longer fit. The colleague dinners at better restaurants. The friend group that vacations together. The neighborhood where people hire cleaners rather than scrub their own tubs. Investopedia identifies social influences as a primary driver of lifestyle creep, with increased exposure to new products and technology shaping spending choices. Year 1 is when you are most vulnerable to this pressure because the raise feels like a ticket into a new social tier, and you spend to validate the admission.

Year 5: The Structural Baseline Phase

By Year 5, the visible upgrades are long forgotten. The couch is no longer new. The car has dents. The apartment feels normal, even small. But your spending has not retreated to pre-raise levels. It has become architecture. The habits formed in Year 1 have crystallized into the invisible scaffolding of your daily life, and you no longer experience them as choices. They are simply how things are.

This is the phase where former luxuries become necessities. As Investopedia describes , lifestyle creep occurs when increased discretionary income leads to spending on former luxuries, inadvertently making them new necessities. The weekly restaurant habit from Year 1 is now the default dinner solution. The house cleaner you hired for a busy month is now a permanent line item. The premium grocery delivery you tried once is now the only way you shop. You cannot imagine going back, not because you are spoiled, but because the old way has been erased from your routine.

The most insidious feature of Year 5 is that your fixed costs have risen to absorb the raise entirely. First Financial Bank’s research confirms that lifestyle creep can lead to living paycheck to paycheck despite having a higher income. Your new baseline requires the new salary just to maintain equilibrium. A job loss, a pay cut, or even a smaller-than-expected bonus creates immediate crisis because there is no slack. The cushion was spent on upgrades that now feel mandatory.

Year 5 also introduces what behavioral economists call hedonic adaptation. The thrill of the better apartment evaporates. The excitement of the restaurant habit fades into mere convenience. You are spending significantly more than you did five years ago, but your subjective happiness has returned to baseline. The raise bought a temporary spike in satisfaction, not a permanent elevation. And because the spending continues while the satisfaction does not, you find yourself chasing the next upgrade—the bigger apartment, the newer car, the more exclusive gym—just to feel the spike again.

The Invisible Pivot Points: Where Year 1 Becomes Year 5

Lifestyle inflation does not announce its transition. It happens at specific pivot points where a temporary upgrade becomes a permanent expectation. Recognizing these pivots in real time is the only way to prevent Year 1 from hardening into Year 5.

The Subscription Migration

In Year 1, you add streaming services, meal kits, and premium apps because you can finally afford them. By Year 5, you have forgotten which ones you actively chose. The stack simply exists, billing quietly while you watch the same three shows on the same two platforms. Common examples of lifestyle creep include having so many subscriptions that you cannot enjoy them all. The migration from active selection to passive maintenance is nearly invisible and costs hundreds per month.

The Convenience Layer

Year 1 introduces convenience spending as a treat: delivery instead of cooking, rides instead of transit, laundry service instead of the laundromat. By Year 5, these conveniences are no longer treats. They are time-saving necessities that you justify by referencing your busy schedule. The irony is that you are often busier because you must work more to pay for the conveniences that save you time. The loop is self-reinforcing and expensive.

The Housing Anchor

Housing is the single largest pivot point. The Year 1 upgrade to a nicer apartment or larger mortgage feels like a reward. By Year 5, that housing cost has become the immovable object around which all other spending orbits. Economic research from the University of Michigan documents that housing difficulties have become the clearest effect of inflation, with rent rising at least 6.1% annually over the last five years. When housing absorbs 35% or more of your income, the remaining 65% feels tight regardless of how large the absolute number is. The raise did not create breathing room. It created a larger anchor.

The “Deserve It” Reflex

In Year 1, you buy something nice because you got a raise. By Year 5, you buy something nice because you had a hard week, because it is Tuesday, because the algorithm showed you something. The justification has decoupled from the income event and attached itself to everyday existence. Empower’s research notes that emotions and social factors can contribute to spending inflation, with a raise at work feeling like an opportunity to spend on treats that result in more expenses not immediately felt. The “deserve it” reflex is the emotional engine that keeps lifestyle inflation running long after the raise has been forgotten.

The 50/50 Rule: A Behavioral Brake on the Creep

The standard advice after a raise is to save a fixed percentage of your income. The problem, as financial planner Michael Kitces has demonstrated , is that saving 10% of your income implicitly means you are spending the other 90%. Every raise thereafter is 90% lifestyle inflation and only 10% progress. The result is that your standard of living rises as fast as your savings, which means the gap between where you are and where you need to be never closes.

The alternative is the 50/50 rule: spend half of every raise, save the other half. This sounds like deprivation, but it is actually the opposite. You still get to upgrade your life. You still get the better apartment, the nicer dinner, the improved wardrobe. But you do so at half the speed, which means your savings grow exponentially while your lifestyle improves linearly. Kitces’s modeling shows that someone starting at a 10% savings rate who saves 50% of every raise will exceed a 20% savings rate within a decade and a 30% rate within two decades, all while feeling like their lifestyle is steadily rising.

The psychological brilliance of the 50/50 rule is that it does not require you to cut current spending. It only requires you to moderate the growth of future spending. You are not going backward. You are simply not accelerating as fast. In Year 1, this means the raise buys a modest upgrade and a meaningful boost to your emergency fund. In Year 5, it means your savings have compounded into genuine security while your lifestyle has still improved—just not to the point of fragility.

How to Audit Your Own Creep Before Year 5

If you are already past Year 1 and suspect the creep has begun, the audit is simple but uncomfortable. It requires comparing your current spending to your pre-raise baseline, category by category, without rationalization.

Start with housing. What percentage of your income does it consume now versus then? If the percentage has risen, housing inflation is eating your raise. Next, review subscriptions and recurring services. Investopedia lists overlapping items at home and unused media as common signs of lifestyle creep. Then examine convenience spending: delivery, rideshare, cleaning services, laundry. These categories often triple after a raise because they feel like time-saving investments rather than discretionary luxuries. Finally, check your savings rate. If you are earning significantly more but saving the same absolute dollar amount, your lifestyle inflation is 100% of the raise.

The goal of the audit is not to shame yourself. It is to identify the pivot points where temporary upgrades became permanent baselines. Once identified, you can reverse them selectively. Maybe the meal kit stays but the premium streaming tier goes. Maybe the apartment stays but the weekly restaurant habit drops to monthly. Fidelity recommends boosting your savings contribution rate each time you receive a raise or bonus, so you do not need to sacrifice anything in terms of your current lifestyle while still saving more. The adjustment happens at the source, before the money ever hits your checking account.

The Year 1 Checkpoint

Before you spend the raise, automate the savings. Increase your 401(k) or savings contribution by half the raise amount before the first paycheck arrives.

Delay the housing upgrade by six months. Prove you can save the new income before you commit to higher fixed costs.

Track convenience spending separately. Delivery, rideshare, and services should be visible, not buried in “food” or “transportation.”

Ask the replacement test: If I lost 20% of my income tomorrow, which of these new expenses would I cut first? The answer reveals what is actually essential.

The Raise Was Real. The Inflation Was Optional.

A raise is a single event. Lifestyle inflation is a thousand small decisions that follow it, each one harmless in isolation, each one building the next floor of a tower that eventually requires the new income just to stand still. Year 1 feels like victory because it is. You worked for that money, and spending some of it on a better life is not a sin. But Year 5 reveals the architecture of those decisions, and by then the scaffolding has been painted to match the walls. You cannot see what is holding you up until it shakes.

The antidote is not asceticism. It is velocity control. Spend half the raise. Save half the raise. Let your lifestyle improve slowly enough that your savings can outrun it. Audit your convenience spending before it becomes your baseline. And remember that the goal of a raise was never just a better apartment or a nicer car. It was security, optionality, and the freedom to handle disruption without panic. If Year 5 leaves you with none of those things, the raise did not fail you. The spending did.

Track one category this week. Compare it to five years ago. That gap is your lifestyle inflation, measured in dollars and cents. It is not too late to narrow it. The next raise is coming. Decide now what percentage of it will actually be yours.